How Iron Condors Generate Income: The Mechanics Explained

If you’ve ever looked at an iron condor and wondered how four options legs can reliably generate cash in your account, this post breaks it down. Iron condors are one of the most widely used premium-selling strategies for a reason: they profit when a stock or index stays within a range. By the time you finish reading, you’ll understand exactly how the income is generated, what drives it, and where the edge actually lives.

What Is an Iron Condor?

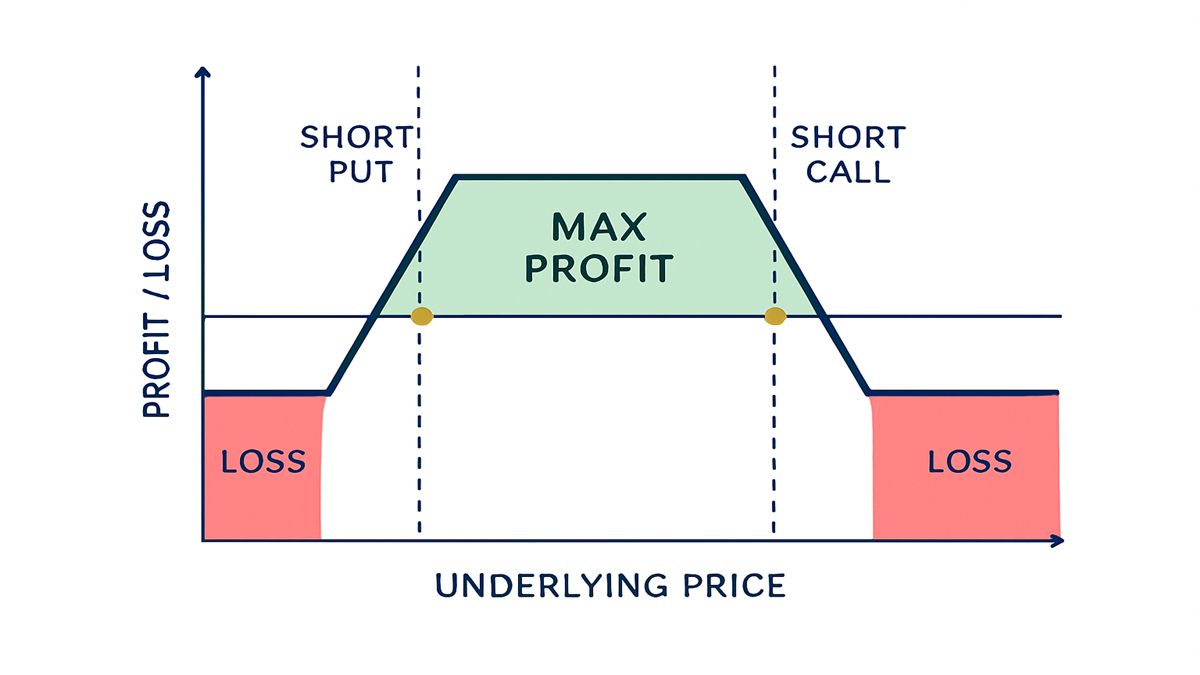

An iron condor is a four-leg options strategy that simultaneously sells two out-of-the-money (OTM) spreads — a put spread below the current price and a call spread above it. You collect a net credit on entry and keep it as long as the underlying closes between your two short strikes at expiration.

The four legs are:

- Sell an OTM put — your lower short strike, where you start to lose if the underlying drops

- Buy a further OTM put — your hedge, which caps your downside loss

- Sell an OTM call — your upper short strike, where you start to lose if the underlying rallies

- Buy a further OTM call — your hedge, which caps your upside loss

The width between your short and long strikes is the spread width. The gap between your two short strikes is your profit zone. The credit collected on entry is the maximum profit you can make on the trade.

Why Iron Condors Generate Income

The income comes from one structural edge: implied volatility (IV) is almost always overpriced relative to what actually happens. Options buyers pay for the possibility of a large move. Options sellers collect that premium and bet the large move won’t materialize — and over hundreds of trades, the market tends to move less than options prices imply.

That persistent gap between implied and realized volatility is where iron condor sellers live. It’s not a guarantee on any single trade. It’s an edge that shows up consistently over a large sample.

Two forces work in your favor once you’re in the position:

- Theta decay — options lose value every day that passes, all else equal. As the seller, time is on your side.

- IV contraction — if implied volatility drops after you enter, the value of your short options decreases. You can buy them back for less than you collected, capturing profit before expiration.

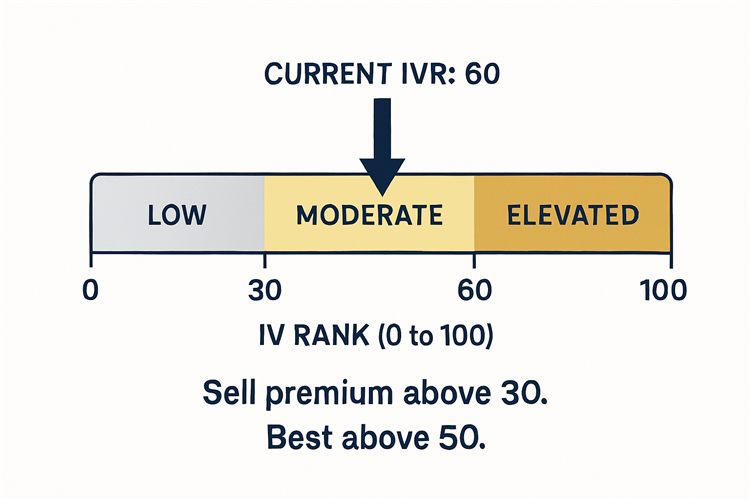

This is why experienced traders filter for elevated IV rank (IVR) before entering iron condors. Selling premium when it’s expensive gives you a wider margin and more credit for the same risk. An IVR above 30 is a reasonable threshold to consider; above 50 is better.

How Iron Condors Work: The Mechanics

Collecting the Premium

When you sell an iron condor, you receive a net credit immediately. This is the combined premium from both short legs minus what you pay for the two long hedges. That credit is yours to keep if the underlying stays inside your profit zone through expiration.

Example: SPY is at $550. You sell the 530/525 put spread and the 570/575 call spread for a combined $1.20 credit. That’s $120 per contract in your account on entry. Your maximum loss is the spread width minus the credit collected: ($5.00 - $1.20) x 100 = $380 per contract.

Your breakeven points are the short strikes plus or minus the credit. In this case, $551.20 on the upside and $528.80 on the downside. Anywhere between those two levels at expiration and you keep some or all of the credit.

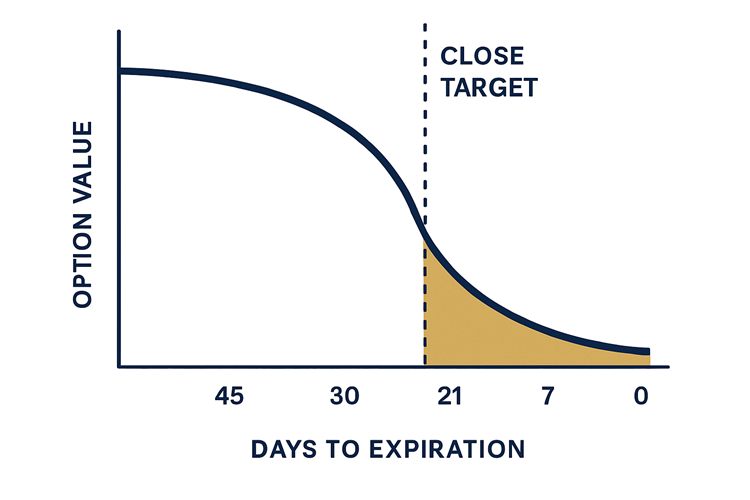

Theta Decay Does the Work

Theta is the daily erosion in an option’s value. It accelerates as expiration approaches, particularly in the final 21 days. This is why most iron condors are entered 30-45 days before expiration (DTE) — you’re positioned to capture the most aggressive part of the decay curve without sitting through slow early erosion.

At 45 DTE, decay is moderate. At 21 DTE, it accelerates significantly. Most systematic traders close iron condors at 50% of max profit or at 21 DTE, whichever comes first. Holding to expiration exposes you to gamma risk — the rapid, unpredictable change in delta as the options approach zero time value. That late-stage volatility is generally not worth the remaining reward.

The Profit Zone

The profit zone is the range between your two short strikes. The underlying can move anywhere inside that range and you keep the full credit. The wider you set your short strikes, the higher your probability of profit — but the lower the credit you collect as a percentage of the spread width.

A typical iron condor on a liquid ETF at 45 DTE targeting the 16-delta on each side (roughly one standard deviation) will have:

- 70-75% probability of profit

- Short strikes about 6-9% away from the current price on each side

- A reward-to-risk ratio around 1:3 (collect $1 to risk $3)

That 70-75% win rate means the trade works roughly three out of four times. The one loss needs to be managed — by rolling, adjusting, or closing — not ignored. See how ACondor manages positions for the approach we use.

IV Rank: Entering at the Right Time

Not all premium is equal. An iron condor entered when IVR is 15 collects thin premium for the same structural risk. The same setup entered at IVR 55 collects substantially more, giving you wider breakeven points and more room for the underlying to move against you.

IVR compares the current IV level to the stock’s IV range over the past 52 weeks. A reading of 60 means IV is in the 60th percentile of where it’s been over the past year — elevated relative to its own history. Selling at high IVR is selling into fear. IV tends to mean-revert downward, which accelerates the value drop in your short options beyond theta alone.

Filtering for IVR is one of the highest-leverage adjustments you can make to a systematic iron condor strategy. It’s built into how ACondor selects trades — see the settings documentation for the full parameter set.

Common Misconceptions About Iron Condors

“You need the stock to stay flat.” Not true. The underlying can move meaningfully in either direction — as long as it stays between your two short strikes. On a liquid ETF with strikes set at one standard deviation, that profit zone is typically 12-18% wide.

“Iron condors always lose in trending markets.” A trending market is harder, but manageable. Entered at high IVR, you have more buffer than you think. The real risk is holding a breached position without a plan. Traders who roll the tested side or close early when a threshold is hit survive trending markets. Traders who freeze do not.

“Higher probability of profit means safer.” Probability of profit is a function of strike selection, not inherent safety. A 90% probability iron condor sounds attractive, but the credit is tiny and the max loss is large relative to the reward. Many experienced traders find that 65-72% probability trades offer better risk-adjusted returns over a large sample. The math matters more than the percentage.

Frequently Asked Questions

How much can you realistically make trading iron condors?

Returns vary by position size, frequency, and management. Systematic iron condor traders typically target 5-10% monthly on buying power used, collected across a portfolio of positions. No single trade defines the outcome — the aggregate over 50-100+ trades does.

What happens if the underlying breaks through a short strike?

The position starts losing value as your short option goes in-the-money. You can roll the tested side to a later expiration for additional credit, close the entire position, or in some cases wait if the breach looks temporary and you still have time. What you should not do is hold to expiration without a plan while the loss grows.

Can you run iron condors on individual stocks?

Yes, but liquidity and earnings risk matter. Stocks can gap significantly overnight on news or earnings, blowing past your strikes with no chance to adjust. Most systematic iron condor traders focus on liquid ETFs — SPY, QQQ, IWM — where spreads are tight and overnight gaps are less extreme.

When is the best time to close an iron condor?

Most traders use a 50% profit target or 21 DTE as their exit trigger, whichever comes first. Closing at 50% of max profit locks in gains and eliminates further exposure. Closing by 21 DTE avoids the sharp gamma risk in the final weeks. Holding for the last few dollars of theta is rarely worth the added risk.

Does position size matter?

Significantly. Each iron condor has a defined max loss. Running too large a position in a single underlying means one bad trade can offset weeks of winning trades. Keeping any single name to 2-5% of total capital is a reasonable starting point for systematic trading.

Ready to Automate Your Options Trading?

ACondor handles iron condors, earnings plays, and volatility strategies automatically in your tastytrade account. No manual entries, no missed setups.

Join the early access list and be first when we open to new accounts.

Ready to Automate Your Options Trading?

ACondor handles iron condors, earnings plays, and volatility strategies automatically in your tastytrade account. No manual entries, no missed setups.

Join the early access list →